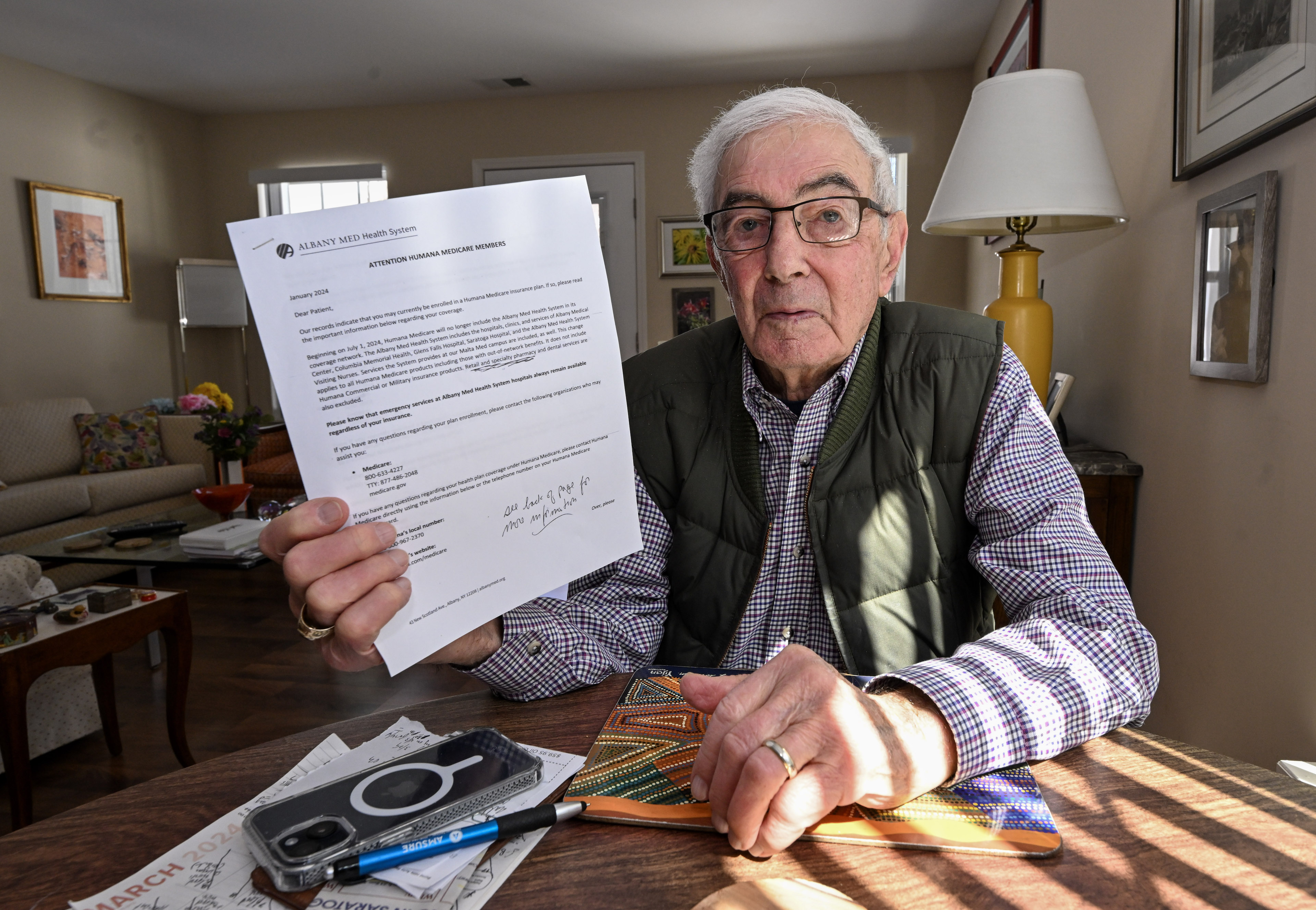

Bart Klion, 95, and his wife, Barbara, faced a tough choice in January: The upstate New York couple learned that this year they could keep either their private, Medicare Advantage insurance plan — or their doctors at Saratoga Hospital.

The Albany Medical Center system, which includes their hospital, is leaving the Klions’ Humana plan — or, depending on which side is talking, the other way around. The breakup threatened to cut the couple’s lifeline to cope with serious chronic health conditions.

Klion refused to pick the lesser of two bad options without a fight.

He contacted Humana, the Saratoga hospital, and the health system. The couple’s doctors “are an exceptional group of caregivers and have made it possible for us to live an active and productive life,” he wrote to the hospital’s CEO. He called his wife’s former employer, which requires its retirees to enroll in a Humana Medicare Advantage plan to receive company health benefits. He also contacted the New York StateWide Senior Action Council, one of the nationwide State Health Insurance Assistance Programs that offer free, unbiased advice on Medicare.

Klion said they all told him the same thing: Keep your doctors or your insurance.

With rare exceptions, Advantage members are locked into their plans for the rest of the year — while health providers may leave at any time.

Disputes between insurers and providers can lead to entire hospital systems suddenly leaving the plans. Insurers must comply with extensive regulations from the Centers for Medicare & Medicaid Services, including little-known protections for beneficiaries when doctors or hospitals leave their networks. But the news of a breakup can come as a surprise.

In the nearly three decades since Congress created a private-sector alternative to original, government-run Medicare, the plans have enrolled a record 52% of Medicare’s 66 million older or disabled adults, according to the CMS. But along with getting extra benefits that original Medicare doesn’t offer, Advantage beneficiaries have discovered downsides. One common complaint is the requirement that they receive care only from networks of designated providers.

Many hospitals have also become disillusioned by the program.

“We hear every day, from our hospitals and health systems across the country, about challenges they experience with Medicare Advantage plans,” said Michelle Millerick, senior associate director for health insurance and coverage policy at the American Hospital Association, which represents about 5,000 hospitals. The hurdles include prior authorization restrictions, late or low payments, and “inappropriate denials of medically necessary covered services,” she said.

“Some of these issues get to a boiling point where decisions are made to not participate in networks anymore,” she said.

An Escape Hatch

CMS gives most Advantage members two chances to change plans: during the annual open enrollment period in the fall and from January until March 31.

But a few years ago, CMS created an escape hatch by expanding special enrollment periods, or SEPs, which allow for “exceptional circumstances.” Beneficiaries who qualify can request SEPs to change plans or return to original Medicare.

According to CMS rules, there’s an SEP patients may use if their health is in jeopardy due to problems getting or continuing care. This may include situations in which their health care providers are leaving their plans’ networks, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

Another SEP is available for beneficiaries who experience “significant” network changes, although CMS officials declined to explain what qualifies as significant. However, in 2014, CMS offered this SEP to UnitedHealthcare Advantage members after the insurer terminated contracts with providers in 10 states.

When providers leave, CMS ensures that the plans maintain “adequate access to needed services,” Meena Seshamani, CMS deputy administrator and director of the federal Center for Medicare, said in a statement.

While hospitals say insurers are pushing them out, insurers blame hospitals for the turmoil in Medicare Advantage networks.

“Hospitals are using their dominant market positions to demand unprecedented double-digit rate increases and threatening to terminate their contracts if insurers don’t agree,” said Ashley Bach, a spokesperson for Regence BlueShield, which offers Advantage plans in Idaho, Oregon, Utah, and Washington state.

Patients get caught in the middle.

“It feels like the powers that be are playing chicken,” said Mary Kay Taylor, 69, who lives near Tacoma, Washington. Regence BlueShield was in a weeks-long dispute with MultiCare, one of the largest medical systems in the state, where she gets her care.

“Those of us that need this care and coverage are really inconsequential to them,” she said. “We’re left in limbo and uncertainty.”

Other breakups this year include Baton Rouge General hospital in Louisiana leaving Aetna’s Medicare Advantage plans and Baptist Health in Kentucky leaving UnitedHealthcare and Wellcare Advantage plans. In San Diego, Scripps Health has left nearly all the area’s Advantage plans.

In North Carolina, UNC Health and UnitedHealthcare renewed their contract just three days before it would have expired, and only two days before the deadline for Advantage members to switch plans. And in New York City, Aetna told its Advantage members this year to be prepared to lose access to the 18 hospitals and other care facilities in the NewYork-Presbyterian Weill Cornell Medical Center health system, before reaching an agreement on a contract last week.

Limited Choices

Taylor didn’t want to lose her doctors or her Regence Advantage plan. She’s recovering from surgery and said waiting to see how the drama would end “was really scary.”

So, last month, she enrolled in another plan, with help from Tim Smolen, director of Washington’s SHIP, Statewide Health Insurance Benefits Advisors program. Soon afterward, Regence and MultiCare agreed to a new contract. But Taylor is allowed only one change before March 31 and can’t return to Regence this year, Smolen said.

Finding an alternative plan can be like winning at bingo. Some patients have multiple doctors, who all must be easy to get to and covered by the new plan. To avoid bigger, out-of-network bills, they must find a plan that also covers their prescription drugs and includes their preferred pharmacies.

“A lot of times, we may get through the provider network and find that that’s good to go but then we get to the drugs,” said Kelli Jo Greiner, state director of Minnesota’s SHIP, Senior LinkAge Line. Since Jan. 1, counselors there have helped more than 900 people switch to new Advantage plans after HealthPartners, a large health system based in Bloomington, left Humana’s Medicare Advantage plans.

Choices are more limited for low-income beneficiaries who receive subsidies for drugs and monthly premiums, which only a few plans accept, Greiner said.

For almost 6 million people, a former employer chooses a Medicare Advantage plan and requires them to enroll in it to receive retiree health benefits. If they want to keep a provider who leaves that plan, those beneficiaries must forfeit all their employer-subsidized health benefits, often including coverage for their families.

The threat of losing coverage for their providers was one reason some New York City retirees sued Mayor Eric Adams to stop efforts to force 250,000 of them into an Aetna Advantage plan, said Marianne Pizzitola, president of the New York City Organization of Public Service Retirees, which filed the lawsuit. The retirees won three times, and city officials are appealing again.

CMS requires Advantage plans to notify their members 45 days before a primary care doctor leaves their plan and 30 days before a specialist physician drops out. But counselors who advise Medicare beneficiaries say the notice doesn’t always work.

“A lot of people are experiencing disruptions to their care,” said Sophie Exdell, a program manager in San Diego for California’s SHIP, the Health Insurance Counseling & Advocacy Program. She said about 32,000 people in San Diego lost access to Scripps Health providers when the system left most of the area’s Advantage plans. Many didn’t get the notice or, if they did, “they couldn’t get through to someone to get help making a change,” she said.

CMS also requires plans to comply with network adequacy rules, which limit how far and how long members must travel to primary care doctors, specialists, hospitals, and other providers. The agency checks compliance every three years or more often if necessary.

In the end, Bart Klion said he had no alternative but to stick with Humana because he and his wife couldn’t afford to give up their retiree health benefits. He was able to find doctors willing to take on new patients this year.

But he wonders: “What happens in 2025?”